If you’re reading this, you’ve made the hardest decision already: you are committed to destroying your debt. But once that commitment is made, a new question arises: How do you actually attack it?

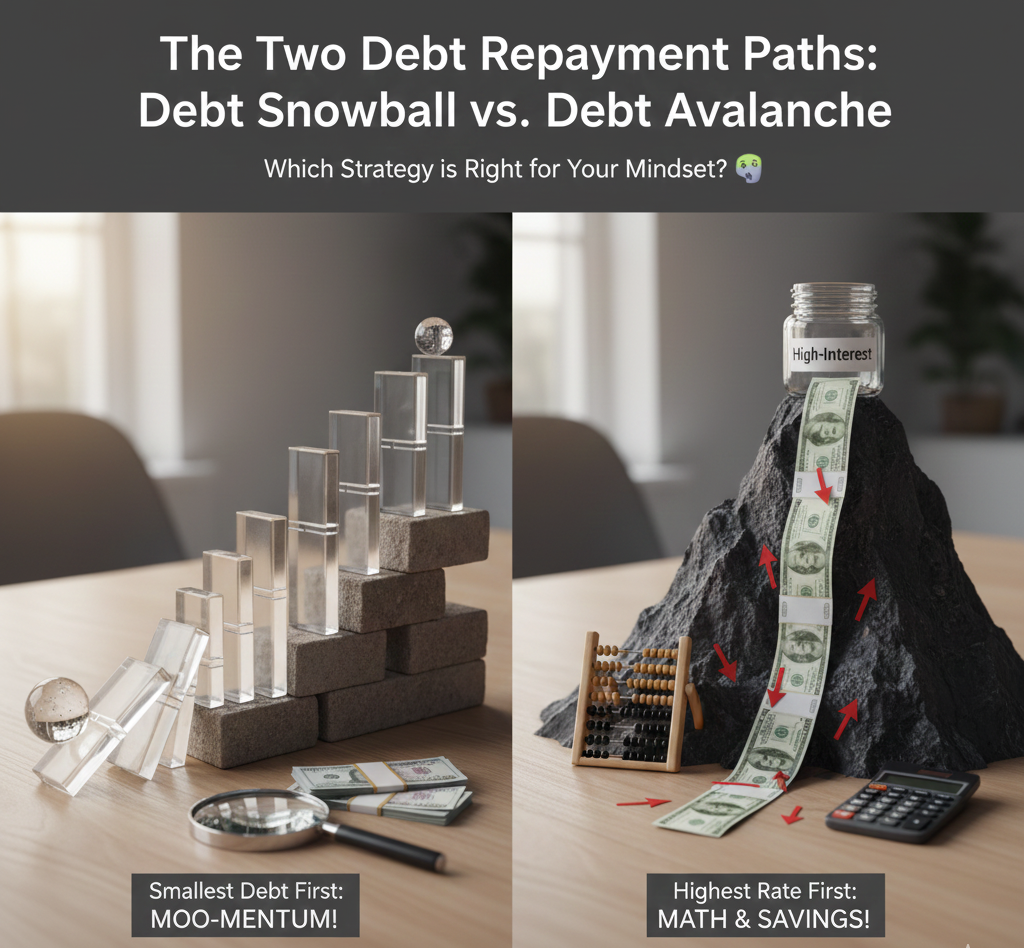

The finance world offers two primary, scientifically-backed methods for organized debt repayment, and they represent a fundamental split: Logic vs. Psychology. These are the Debt Avalanche and the Debt Snowball.

Both methods work brilliantly, but one is mathematically superior, and the other is psychologically superior. Understanding the difference is critical, because the best method for you is the one you will actually stick with until the last balance is gone.

🏔 The Debt Avalanche: Minimizing the Cost

The Debt Avalanche is the mathematically superior method. This strategy treats debt like a calculated financial foe, prioritizing the highest cost first.

How the Avalanche Works

- List all your debts from highest interest rate (APR in the UK, or just the interest rate in the US) to lowest. Ignore the balances completely-only the rate matters here.

- Make minimum payments on every single debt except the top one (the highest rate).

- Throw every extra penny you can into the debt with the highest interest rate.

- Once that highest-rate debt is completely paid off, you take the money you were paying on it and apply it to the next debt on your list (the one with the second-highest rate).

- Repeat until you are debt-free.

Who the Avalanche is For

The Debt Avalanche is ideal for the analytical, disciplined reader-the person who can see the big picture and prioritize long-term savings over short-term wins. If you are detail-oriented, have high-interest student loans or credit card balances, and can stay motivated by watching the total interest saved rather than the balance drop, this is your path.

The Bottom Line: You pay the least amount of interest possible, making this the cheapest option over time.

☃ The Debt Snowball: Building the Momentum

The Debt Snowball is the psychologically superior method. This strategy focuses on building momentum, prioritizing the emotional lift of quick wins.

How the Snowball Works

- List all your debts from smallest balance to largest. Ignore the interest rates completely-only the balance matters here.

- Make minimum payments on every single debt except the top one (the smallest balance).

- Throw every extra penny you can into the debt with the smallest balance.

- Once that smallest debt is completely paid off, you take the entire previous payment (the payment amount plus the extra you were paying) and apply it to the next smallest debt. This is the snowball effect.

- Repeat until you are debt-free.

Who the Snowball is For

The Debt Snowball is perfect for the reader who needs quick wins to stay motivated. If you’ve struggled to stick with budgets before, or if seeing a balance hit zero gives you a massive psychological lift, the Snowball is your best bet. It leverages human behavior-the excitement of crossing a finish line-to keep you committed.

The Bottom Line: You feel results faster, which dramatically increases the likelihood you will complete the plan.

🇺🇸 / 🇬🇧 The Debt Landscape: Knowing Your Enemy

The principles are universal, but the types of debt we often face in the USA and UK differ slightly, especially when discussing student loans, which are a common feature of the debt landscape.

| Debt Type | USA Focus | UK Focus |

| High-Interest Debt | Credit Card balances, Private Student Loans, Personal Loans. | Credit Card balances, High-rate Personal Loans. |

| Common Low-Rate Debt | Federal Student Loans (often lower interest than credit cards). | Mortgages (secured debt), Student Loans (rate dependent on plan type and income). |

| Strategy Note | For the Avalanche, prioritize any debt over 10% interest first. | Consider whether your UK student loan is “real debt” for budgeting purposes. If payments are income-dependent, you might prioritize other debt first. |

Human Insight: When listing your debts for the Snowball method, remember that Credit Score management (USA FICO, UK Experian/Equifax) is a factor. Clearing small, revolving debt balances like credit cards can give a healthy boost to your score quickly, which is a nice side benefit of the Snowball.

The Verdict: Logic vs. Psychology

Which method should S.M. Guide readers choose?

| Factor | Choose Avalanche If… | Choose Snowball If… |

| Goal | Saving the most money possible (the most logical choice). | Gaining momentum and staying motivated (the most psychological choice). |

| Your Debt | You have large balances with widely varying, high interest rates (e.g., 25% credit card and 7% personal loan). | You have many small balances that can be cleared quickly, giving you fast wins. |

| Your Mindset | You are highly disciplined and focused on the final number. | You struggle with long-term commitment and need immediate gratification to keep going. |

If you are wavering, I would almost always recommend the Debt Snowball first. Why? Because the money you lose in extra interest is often a small price to pay for the behavioral training and psychological reinforcement you gain by successfully completing the program. The best debt strategy is the one you don’t quit.